Crisis and Caution: Personal Finance in USA 2026’s Unpredictable Landscape

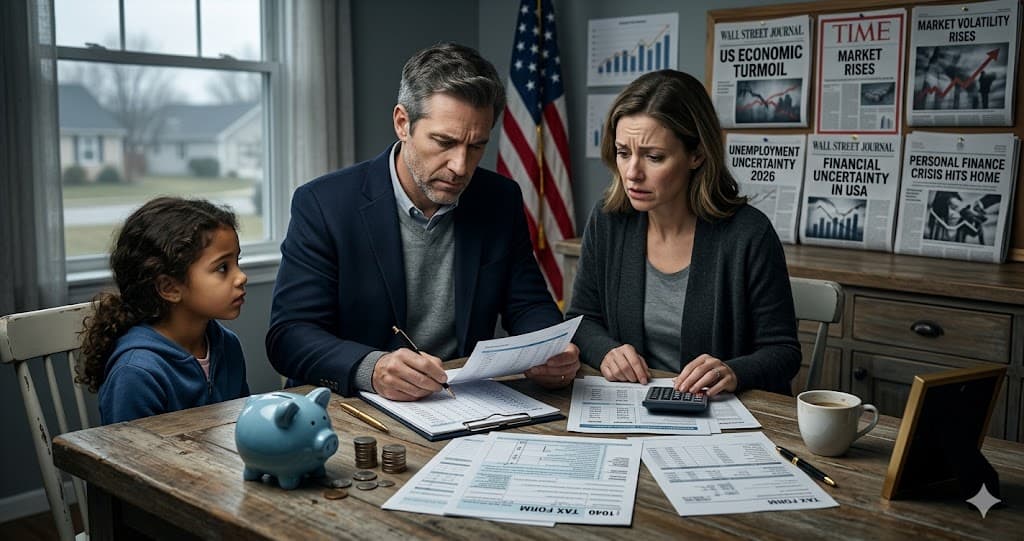

As we navigate the first quarter of 2026, the landscape of personal finance USA 2026 is characterized by a unique blend of geopolitical tensions, persistent inflation, and evolving consumer behaviors. Recent events and market indicators paint a picture of an economy demanding vigilance and adaptability from individuals. From the fallout of international conflicts on retirement savings to shifts in everyday spending habits, understanding these current realities is paramount for effective financial management.

The imperative to budget savings effectively in the USA for 2026 remains strong. Financial experts continually advise prioritizing saving a portion of income before spending, exploring cost-effective alternatives for daily expenses, and staying informed about market trends to make financially sound decisions. This advice is particularly salient given the current climate, as we delve into the specific ‘breaking news’ and ‘current situations’ shaping the American financial experience.

Geopolitical Tensions and Their Immediate Impact on Markets

One of the most significant and unsettling developments impacting personal finance in early 2026 is the ongoing U.S. war with Iran. The ripple effects of this conflict are tangible, reaching directly into the retirement accounts of everyday Americans. As noted by Washington Post columnist Michelle Singletary in September 2025, she unexpectedly witnessed a “significant decline” in her own retirement account balance, directly attributing it to “the fallout from the U.S. war with Iran.” This personal anecdote underscores a broader market reality: geopolitical instability directly translates into market volatility.

Singletary’s experience serves as a stark reminder of the advice she frequently offers: it’s “best to avoid fear-driven trades in a roller-coaster stock market.” This counsel is more pertinent than ever, as news from March 24, 2026, indicates that Army paratroopers have been ordered to the Middle East, signaling the U.S. is weighing its next moves in the ongoing Iran conflict. Such developments inherently create an environment of uncertainty, influencing investor confidence and market performance. For individuals, this means retirement portfolios and other investments are subject to fluctuations driven by global events, emphasizing the need for a long-term perspective and disciplined financial planning rather than reactive decisions.

Beyond investment portfolios, the war’s impact is felt directly in household budgets through soaring energy costs. By March 26, 2026, fuel prices were reported to be “nuzzling up to $9 a gallon in California,” a direct consequence of the conflict and broader market dynamics. This dramatic increase in transportation costs has a cascading effect, increasing the cost of goods and services across the board and further tightening household budgets already strained by inflation. The interplay between geopolitical events and everyday expenses highlights the interconnectedness of the global economy and individual financial well-being.

Persistent Inflation and the Rising Cost of Living

The specter of inflation continues to loom large over personal finance in the USA in 2026. Evidence from various sectors points to a sustained period of higher costs, affecting everything from essential services to consumer goods. On March 26, 2026, the U.S. Postal Service announced an 8% hike in prices for popular services, citing “rising transportation costs.” This is a direct example of how increased operational expenses, often tied to fuel prices and supply chain pressures, are passed directly onto consumers, making everyday tasks more expensive.

This trend of escalating costs is not new. As far back as December 2025, reports indicated that “Higher costs push holiday shoppers toward socks, coffee and diapers,” signifying a shift towards necessity-driven purchases over discretionary spending. This pivot in consumer behavior is a clear indicator that households are feeling the squeeze, adapting their purchasing patterns to prioritize essential items. The overall economic environment, characterized by rising prices for basic necessities, forces individuals to re-evaluate their spending habits and seek out greater efficiencies in their budgets.

The broader economic sentiment around inflation is further complicated by political commentary and market analysis. March 26, 2026, saw discussions around what some experts are calling a “Trump market,” suggesting that traditional bull or bear market definitions no longer fully capture the current economic dynamics. This unique market environment, influenced by political rhetoric and policy, adds another layer of complexity for individuals trying to make sense of economic forecasts and plan their finances. The implication is that conventional wisdom might need to be adjusted to navigate this “Trump market,” which could introduce new risks and opportunities for investors and consumers alike.

Shifting Consumer Behaviors: The Era of Frugality and Strategic Spending

In response to market volatility and persistent inflation, American consumers are increasingly embracing strategies of frugality and disciplined spending. This shift is evident in several key trends observed throughout late 2025 and early 2026. Michelle Singletary’s column from September 2025 explicitly sought readers’ “most frugal-to-a-fault strategies,” highlighting a popular interest in extreme saving hacks. This public discourse around cost-cutting reflects a widespread need and desire to manage finances more tightly.

A significant manifestation of this trend is the “no buy” movement, which, as Singletary noted in June 2025, “sparks a rebellion against spending.” This movement encourages individuals to drastically reduce or eliminate non-essential purchases for a set period, forcing a re-evaluation of consumption habits. Such movements gain traction when economic conditions necessitate greater financial discipline, demonstrating a collective effort by consumers to regain control over their expenditures in a challenging environment.

Moreover, the economic pressure is particularly acute for certain demographics. Reports from September 2025 indicated that “Low-income Americans slash spending, a worrying sign for the economy.” This behavior, while a rational response to financial constraints, can have broader economic implications, as reduced consumer spending can slow economic growth. However, for the individuals themselves, it represents a necessary adaptation to higher costs and stagnant wages, emphasizing the importance of finding “cost-effective alternatives for daily expenses like dining out and travel,” a tip consistently reiterated by financial advisors.

Even in areas traditionally associated with significant spending, such as home improvement, there’s an underlying current of strategic investment. Grand Building Construction, for instance, announced an expansion of its home remodeling services across Greater Seattle in March 2026. While this might seem contradictory to a “no buy” philosophy, it often represents a different kind of financial decision: investing in existing assets to increase their value or improve living conditions, rather than purely discretionary spending. This kind of “value-add” spending often aligns with long-term financial health goals, which include maintaining asset value and planning for future expenses, as recommended by general financial advice.

Navigating the Investment Landscape: Opportunities and Warnings

Despite the prevailing market volatility, the investment landscape in 2026 continues to present both challenges and specific opportunities. The cryptocurrency market, for instance, remains a notable area of activity. iTrustCapital, a crypto IRA provider, launched its “Conquest Program” in March 2026, offering new clients a 2% match bonus for transferring assets from other providers. This indicates a continued, albeit perhaps more cautious, interest in digital assets as part of a diversified investment strategy, particularly within tax-advantaged retirement accounts.

However, the broader financial markets are still in flux. Current prices for key commodities and assets like Bitcoin and oil are being closely watched. Fortune reported the “Current price of Bitcoin for March 26, 2026” and the “Current price of oil as of March 26, 2026,” underscoring the daily volatility and the need for investors to stay informed. This constant fluctuation, particularly in sectors tied to global events and supply chains, reinforces Michelle Singletary’s advice to avoid “fear-driven financial decisions during market volatility.” Instead, a disciplined approach, focusing on long-term goals rather than short-term swings, is crucial.

The commentary from March 26, 2026, suggesting “We’re no longer in a bull or bear market. We’re in a Trump market — and here’s how to navigate it,” further complicates investment strategies. This “Trump market” implies a unique set of drivers and sensitivities that may defy traditional economic models, requiring investors to be particularly agile and well-informed. Understanding these specific market dynamics, whether influenced by geopolitical events, domestic policy, or public sentiment, is critical for making sound investment choices in 2026.

Long-Term Financial Health: Social Security and National Solvency Concerns

Beyond immediate market fluctuations and consumer spending, underlying structural issues in the U.S. economy continue to pose significant long-term challenges for personal finance. One of the most pressing concerns is the solvency of Social Security. A Fortune article from March 24, 2026, highlighted discussions around “Social Security insolvency,” exploring how a ‘six figure cap’ on benefits for the ultra-wealthy “could buy the program 7 critical years.” This ongoing debate about the future of Social Security directly impacts millions of Americans who rely on it for retirement income, necessitating proactive planning for future expenses and retirement savings.

Perhaps even more alarming was the Fortune report from March 23, 2026, stating, “The Treasury just declared the U.S. insolvent.” While the nuances of such a declaration require careful interpretation, the headline itself signals a profound concern about the nation’s financial health. For the average American, a declared “insolvency” by the Treasury, even if technically referring to specific financial obligations rather than outright bankruptcy, casts a shadow of uncertainty over the stability of the broader economic system. This kind of high-level financial news, even when complex, resonates with individuals and can influence their long-term financial planning, potentially prompting a greater focus on personal savings and diversification of assets.

These discussions around national solvency and the future of critical social programs underscore the importance of “focus[ing] on long-term financial health by managing debt and planning for future expenses,” as emphasized in the general budgeting advice for 2026. Individuals must consider how these larger economic trends might affect their retirement, healthcare costs (especially with discussions around Medicaid strength as seen in March 2026), and overall financial security, prompting a more robust approach to personal financial planning.

The Evolving Workplace and Economic Sentiment

The dynamics of the American workforce also contribute to the current personal finance landscape. JPMorgan CEO Jamie Dimon’s comments on March 25, 2026, regarding remote work, where he suggested it “breeds ‘rope-a-dope politics’ and stunts young workers’ growth,” highlight ongoing debates about productivity, career development, and the future of work. These discussions are critical for individuals planning their careers, assessing earning potential, and understanding the evolving demands of the job market. The shift in work modalities, whether towards or away from remote work, has direct implications for household budgets (e.g., commuting costs, home office expenses) and long-term career trajectories.

Overall economic sentiment, as influenced by these diverse factors, plays a significant role in consumer and investor confidence. The combination of geopolitical conflict, inflationary pressures, and discussions around national solvency creates a climate of caution. Even positive news, such as breakthroughs in technology or niche market expansions (like Winston Self Storage’s expansion in March 2026, reflecting demand for flexible space, or Eternity.Photos’ archival service), exists within this broader context of uncertainty. People are looking for stability and security, leading to increased demand for services that offer safety and preservation, whether for physical goods or digital memories.

Conclusion: Navigating the Complexities of Personal Finance in USA 2026

The current situation for personal finance in the USA in 2026 is undeniably complex, shaped by a confluence of “breaking news” and “current situations.” From the immediate impacts of international conflicts on investment portfolios and fuel prices to the persistent challenges of inflation and the shifting sands of consumer behavior, Americans are navigating an unpredictable financial landscape. The discussions around Social Security solvency and the alarming “U.S. insolvent” statement from the Treasury add layers of long-term concern that demand attention and strategic planning.

In this dynamic environment, the foundational principles of personal finance – disciplined saving, informed decision-making, and a focus on long-term health – are more critical than ever. Individuals are increasingly embracing frugality and seeking cost-effective alternatives, adapting to a new economic reality. Staying informed about market trends, understanding the implications of geopolitical events, and proactively managing debt and future expenses will be key to financial resilience and success in the continuing fiscal year.